What is the difference between flood insurance that is unaffordable vs. a house that is uninsurable?

Not much to a resident.

Premiums are doubling, tripling or more since the 2022 floods across Australia.

Some people say ‘this is unacceptable, people need insurance’.

Others say ‘this is the market working, the price reflects the risk of living in these areas’.

But how do we square the availability of insurance and the safety that its offers, with the lifetime project of adapting and weathering an increasingly volatile climate?

I have been reading Understanding Disaster Insurance: New Tools for a More Resilient Future by Carolyn Kousky.

I wanted to set out some of the key takeaways.

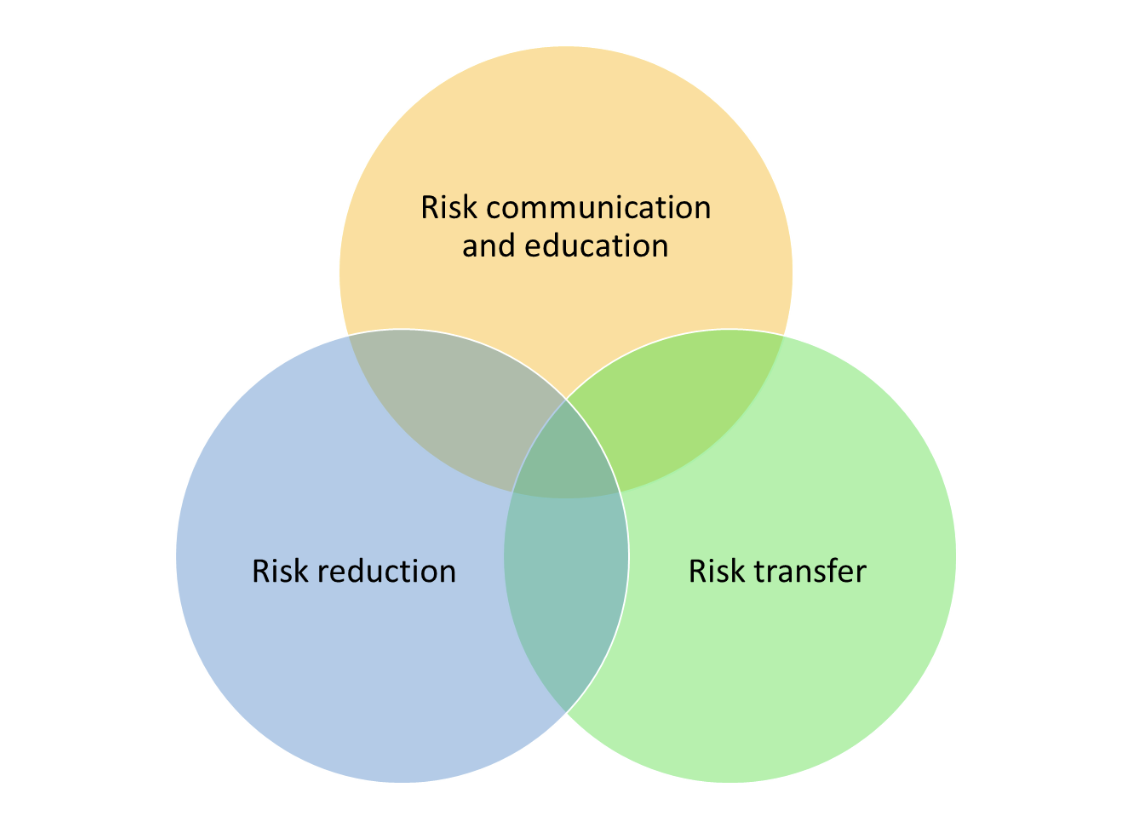

1. Three interlocking concepts make up risk management

- Risk communication and education: what residents, developers, government and the broader community understand about the risks to them from disasters and what they understand that they can do about it

- Risk transfer: transference of risk to other parties (i.e. risk assumed by insurance or government socialised risk programs)

- Risk reduction: actions taken to the reduce the likelihood and impact of disasters

Three areas of risk management work together to build greater resilience

2. Humans do not intuitively understand the probabilistic modelling of flood risk

- A home in a one-hundred year flood plain.

- A home where there is a 1 percent chance of flooding each year.

- A home with a more than 1-in-4 chance of a flood at least once over a 30 year mortgage.

Which is more likely to flood?

Trick question — they are all expressing the same risk.

Communication matters.

I am not sure that I want a 1-in-4 chance of at least one flood over the lifetime of my mortgage.

Our understanding of risk not just impacted by the way that things are presented but also by our memories. We over-emphasis the most recent history in our assessment of risk.

3. Climate change makes flood risk even more difficult to communicate, reduce and transfer.

Climate change makes this worse because:

- By its very nature, climate change is an increase in atmospheric energy (i.e. temperature is just a measurement of energy) so every modelled disaster has to be sized up. A 1% AEP flood has to higher each year that the energy in the atmosphere increases (ceteris paribus).

- It is continuing to increase as global emissions increase.

- It is not going to ‘go down’ in impact in our lifetimes without major geoengineering.

So risk transfer has to become more costly as the pure risk (likelihood and impact) increases. Risk reduction will not reduce ‘as much’ risk with the same amount of investment.

Risk communication and education has to ‘update’ people’s assumptions rather than build a static picture of risk.

4. Self-insurance is not an efficient mechanism for managing flood risk?

‘Well if I can’t insure my house, then I will just adapt my house and then have a specific amount of savings for flood recovery’.

The book states that

There is a robust body of literature indicating that individuals and communities with insurance recover better and faster from disaster events than those without insurance.

So it is not clear that self-insurance is efficient – communities do not do better under self-insurance.

Is it better for individuals? Maybe as part of a diversified strategy for high income people with lots of financial resilience.

5. Feels inevitable that we will ‘socialise’ the risk.

There is conflict about whether the withdrawal of insurance is:

a) a market clearing action signalling where people can live and be insured, or

b) the withdrawal creates negative externalities which should be mitigated by socialising the risk from insurers to governments (and ultimately taxpayers or lower risk residents).

Reading about socialising the risk examples of Florida Citizens Insurance, Flood Re in the UK, FAIR wildfire insurance in California and cyclone insurance in Australia left many questions:

- Why do some socialising risk vehicles (i.e. Florida Citizens and Flood Re) have termination dates of 2039?

- What is the benefit of Florida Citizens now being the only hurricane/wind insurer of any size in Florida?

- What is acceptable risk reduction by policy holders of insurance products linked to socialised risk vehicles?

The book says that politicians prefer cheaper insurance in high-risk areas even if those in lower-risk areas must pay for it. It must be the case that those who can access insurance via socialised risk vehicles will have strong thoughts about any changes that reduce their access or cover.

Parametric insurance, where payouts are linked to particular disaster attributes, look alot like the emergency triggers which push support money out to affected people.

6. My other thoughts

- What is the impact of extending insurance products beyond one year do for risk transfer decisions and ultimately risk exposure? Would we build in flood prone areas if insurance had to be five years or more as well as being mandatory?

- Disaster insurance is only going to get more complex. Overlapping private insurance with government pools, risk reduction activity mandates and ongoing legal challenges in the aftermath of disasters; whatever we deal with today will be considered ‘simple’ in 5-10 years time.

- This increase in complexity will, at the very least, increase administration costs for insurers so premiums will increase on this basis alone.

- Flood risk re-evaluators may arise to negotiate with insurers on resident’s behalf (new climate jobs!)

- Traditional insurance will be layered with parametric risk — a payout triggered by a moderate flood level on the St Lucia river gauge?

- The business model vs. breaking down the obstacles to insurance in a climate affected world conundrum is not closer to be resolved. Each innovation seems to be at odds with the 300 year old business model of writing policies that result in net profits to insurers.

Kousky’s book says that it is a moment of deep change insurance, but the only stated innovations are VC backed ‘smart insurance’ that mainly delivers on reduced costs through automation.

Other than that, it is hard to square the severity of the situation with the plodding nature of insurance.

Written by Sebastian Vanderzeil, Resilient Kurilpa & WECA

Article originally published on Strabo’s Delta and Resilient Kurilpa.

Cover image iStock – ARK Photography